32 Visualizing Time Series Data

Kate Lassiter

32.0.0.1 Starting Point

Same exploratory questions as with any new data set:

- Strongly correlated columns

- Variable means

- Sample variance, etc.

Use familiar techniques:

- Summary statistics

- Histograms

- Scatter plots, etc.

Be very careful of lookahead!

- Incorporating information from the future into past smoothing, prediction, etc. when you shouldn’t know it yet

- Can happen when time-shifting, smoothing, imputing data

- Can bias your model and make predictions worthless

32.0.0.2 Working with time series (ts) objects

Integration of ts() objects with ggplot2:

- ggfortify package

- autoplot()

- All the same customizations as ggplot2

- Don’t have to convert from ts to dataframe format

- gridExtra package

- Arrange the 4 ggplot plots as a 4-panel grid

- grid package

- Add title to the grid arrangement

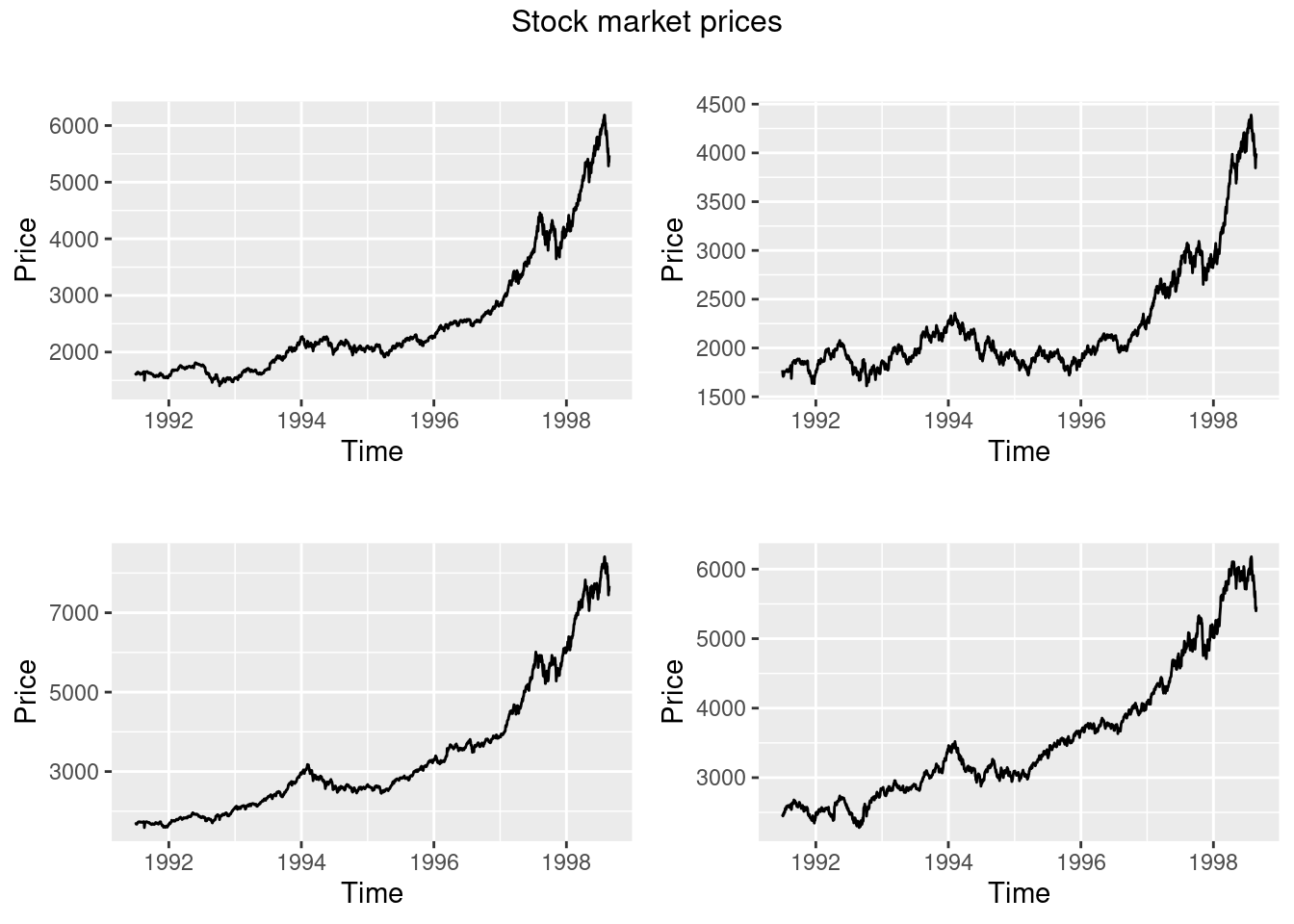

dax=autoplot(EuStockMarkets[,"DAX"])+

ylab("Price")+

xlab("Time")

cac=autoplot(EuStockMarkets[,"CAC"])+

ylab("Price")+

xlab("Time")

smi=autoplot(EuStockMarkets[,"SMI"])+

ylab("Price")+

xlab("Time")

ftse=autoplot(EuStockMarkets[,"FTSE"])+

ylab("Price")+

xlab("Time")

grid.arrange(dax,cac,smi,ftse,top=textGrob("Stock market prices"))

32.0.0.3 Time series relevant plotting:

Working with the data:

- Directly transforming ts() objects for use with ggplot2:

- complete.cases() to easily remove NA rows - prevent ggplot warning

- avoid irritations of working with ts objects

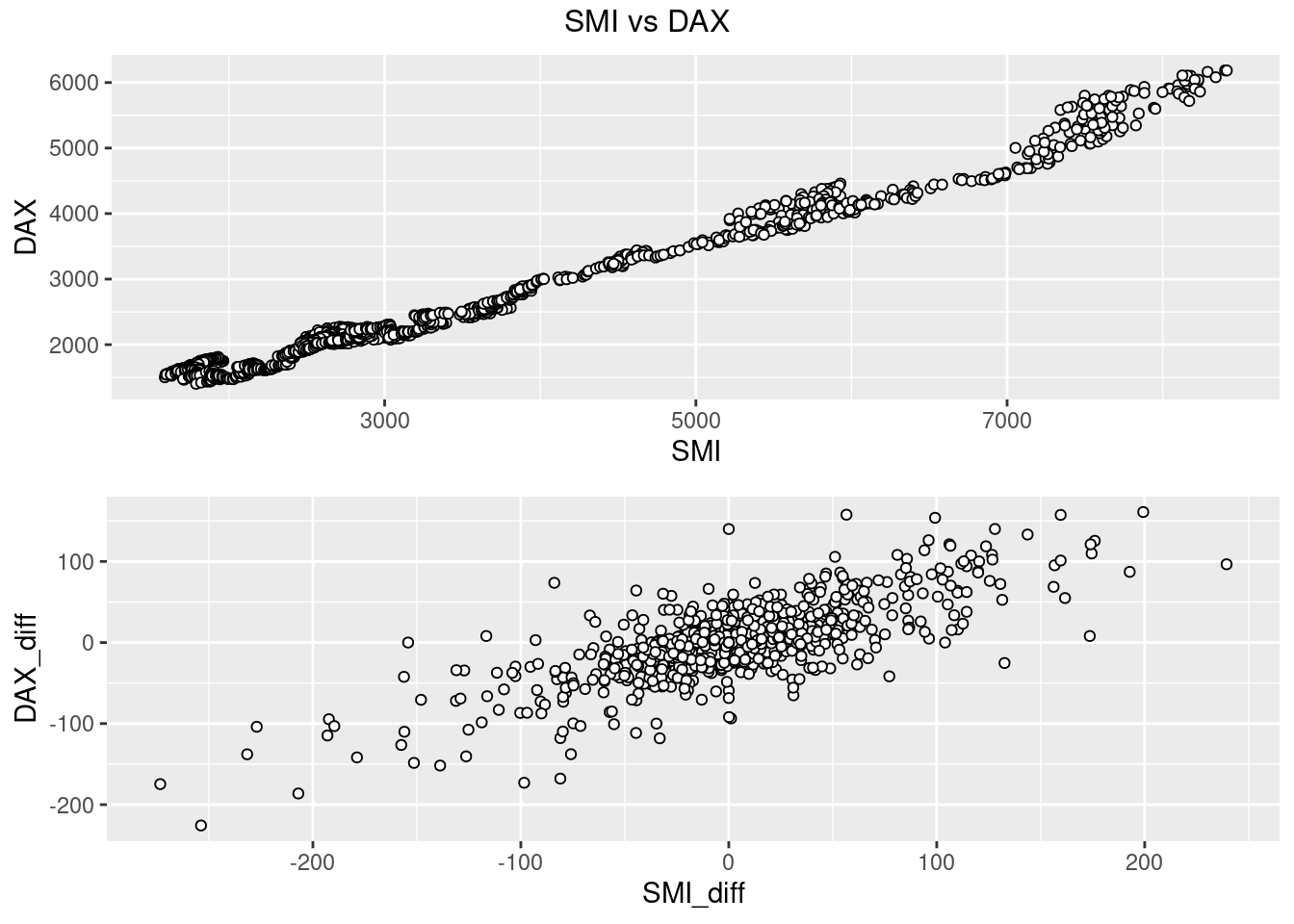

Looking at changes over time:

- Plot differenced values

- Histogram/scatter plot of the lagged data

- Shows change in values, how values change together

- Trend can hide true relationship, make two series appear highly predictive of one another when they move together

- Use base package diff(), calculates difference between point at time t and t+1

new=as.data.frame(EuStockMarkets)

new$SMI_diff=c(NA,diff(new$SMI))

new$DAX_diff=c(NA,diff(new$DAX))

p1 <- ggplot(new, aes(SMI,DAX))+

geom_point(shape = 21, colour = "black", fill = "white")

p2 <- ggplot(new[complete.cases(new),], aes(SMI_diff,DAX_diff))+

geom_point(shape = 21, colour = "black", fill = "white")

grid.arrange(p1,p2,top=textGrob("SMI vs DAX"))

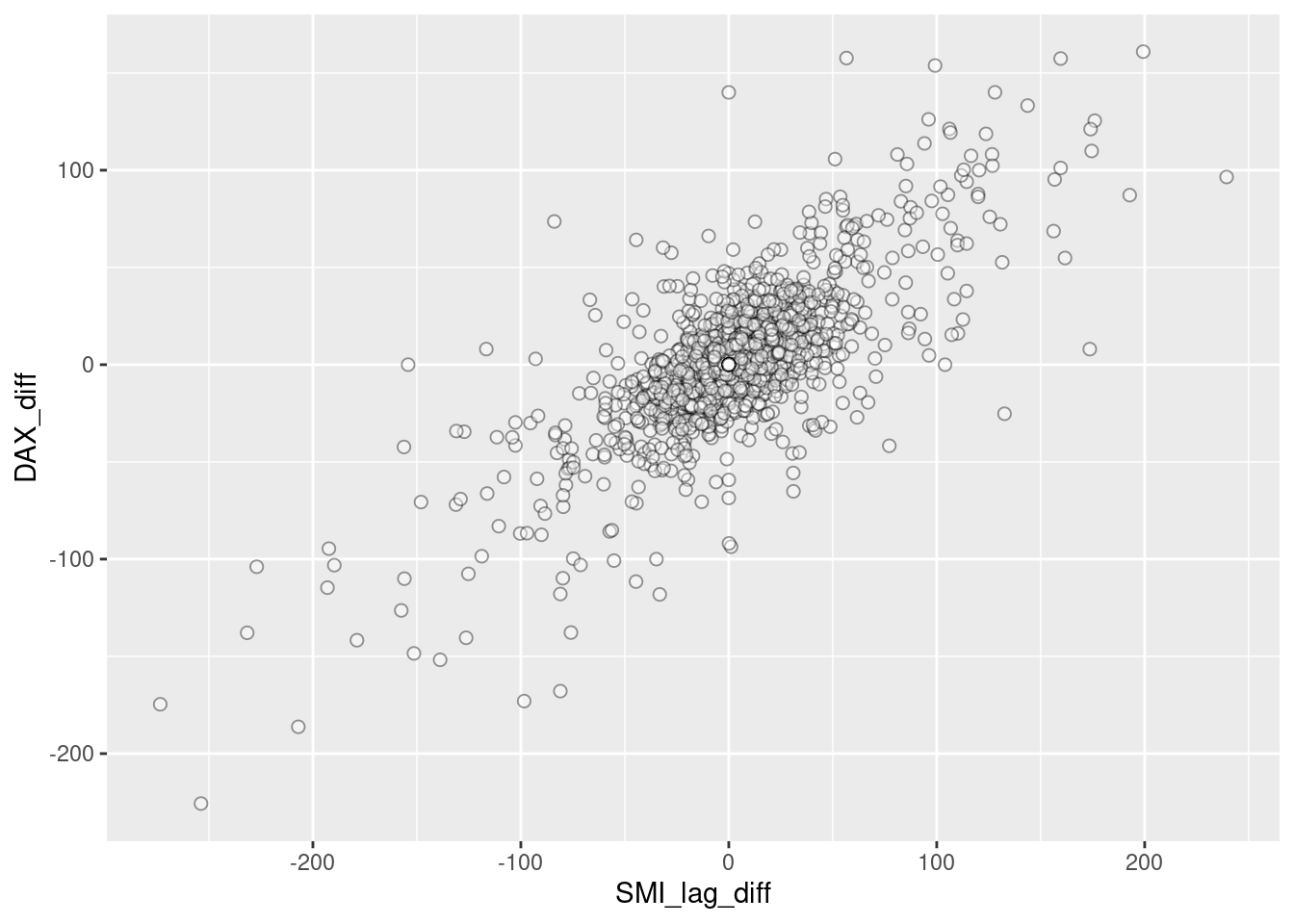

Exploring Time Lags:

- Lagged differences:

- Time series analysis: focused on predicting future values from past

- Concerned whether a change in one variable at time t predicts change in another variable at time t+1

- lag() to shift forward by one

- Showing density using alpha

new$SMI_lag_diff=c(NA,lag(diff(new$SMI),1))

ggplot(new[complete.cases(new),], aes(SMI_lag_diff,DAX_diff))+

geom_point(shape = 21, colour = "black", fill = "white",alpha=0.4,size=2)

Now there is no apparent relationship: positive change in SMI today won’t predict positive change in DAX tomorrow. There is a positive trend over the long term, but this does little to predict in the short term

Observations:

- Be careful with time series data: use same techniques, but reshape data

- Change in values from one time to another is vital concept

32.0.0.4 Dynamics of Time Series Data

Three aspects of time series data:

- Seasonal:

- Recurs over a fixed period

- Cycle:

- Recurrent behaviors, variable time period

- Trend:

- Overall drift to higher/lower values over a long time period

- Overall drift to higher/lower values over a long time period

32.0.0.4.1 Line plots

Discover patterns through visual inspection:

- Observations:

- Clear trend

- Consider log transform or differencing

- Increasing variance

- Consider log or square root transform

- Multiplicative seasonality

- Seasonal swings grow along with overall values

- Clear trend

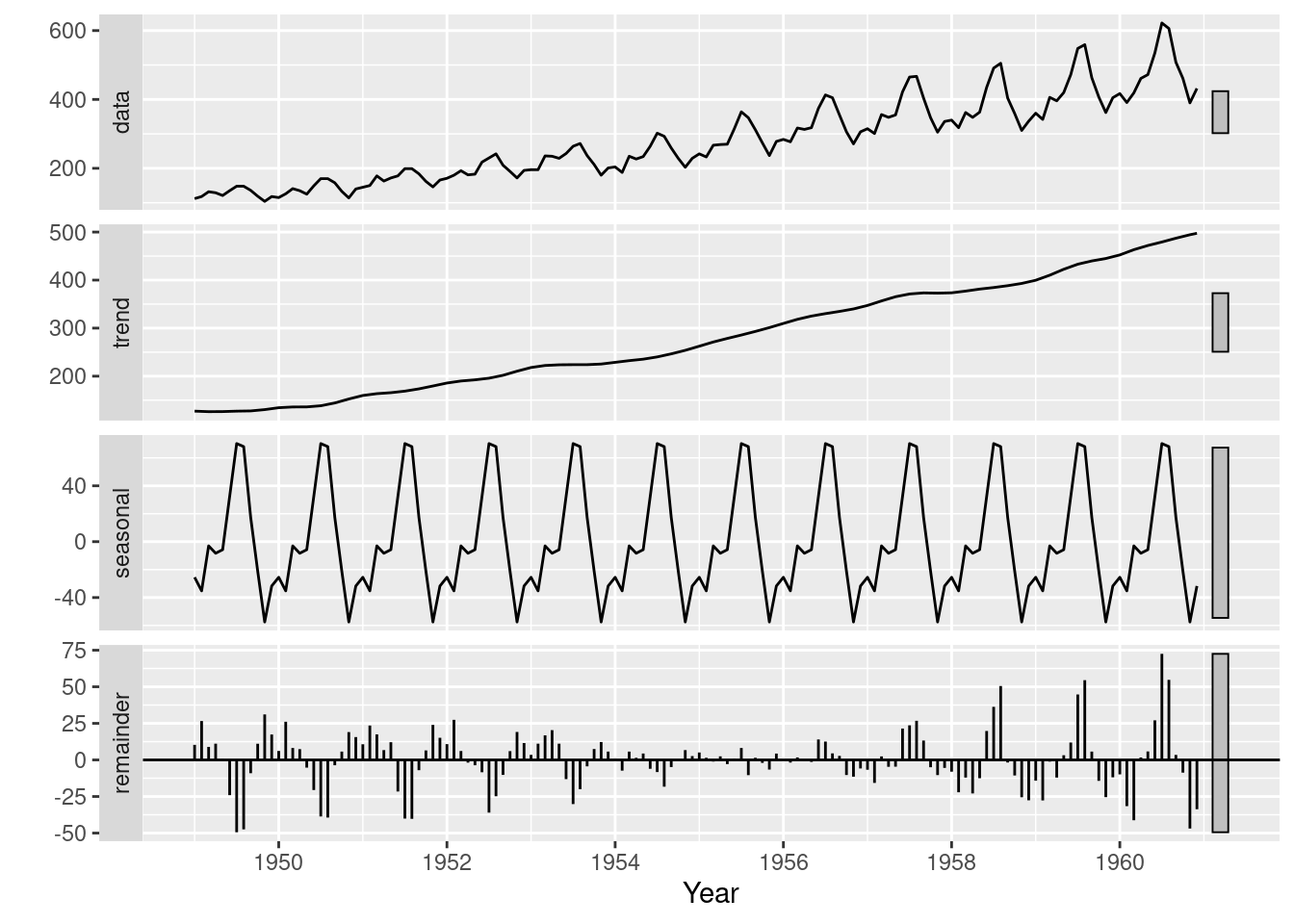

32.0.0.4.2 Time series decomposition:

- Break data into seasonal, trend, and remainder components

- Seasonal component:

- LOESS smoothing of all January values, February values, etc.

- Moving window estimate of smoothed value based on point’s neighbors

- stats package

- stl()

- stl()

- Observations

- Clear rising trend

- Obvious seasonality

- Difference between the two methods:

- This particular decomposition shows additive, not multiplicative seasonality

- But start and end time series have highest residuals

- Settled on the average seasonal variance

- This particular decomposition shows additive, not multiplicative seasonality

- Both reveal information on patterns that need to be identified and potentially dealt with before forecasting can occur

32.0.0.5 Plotting: Exploiting the Temporal Axis

32.0.0.5.1 Gannt charts

- Shows overlapping time periods, duration of event relative to others

- timevis package timevis()

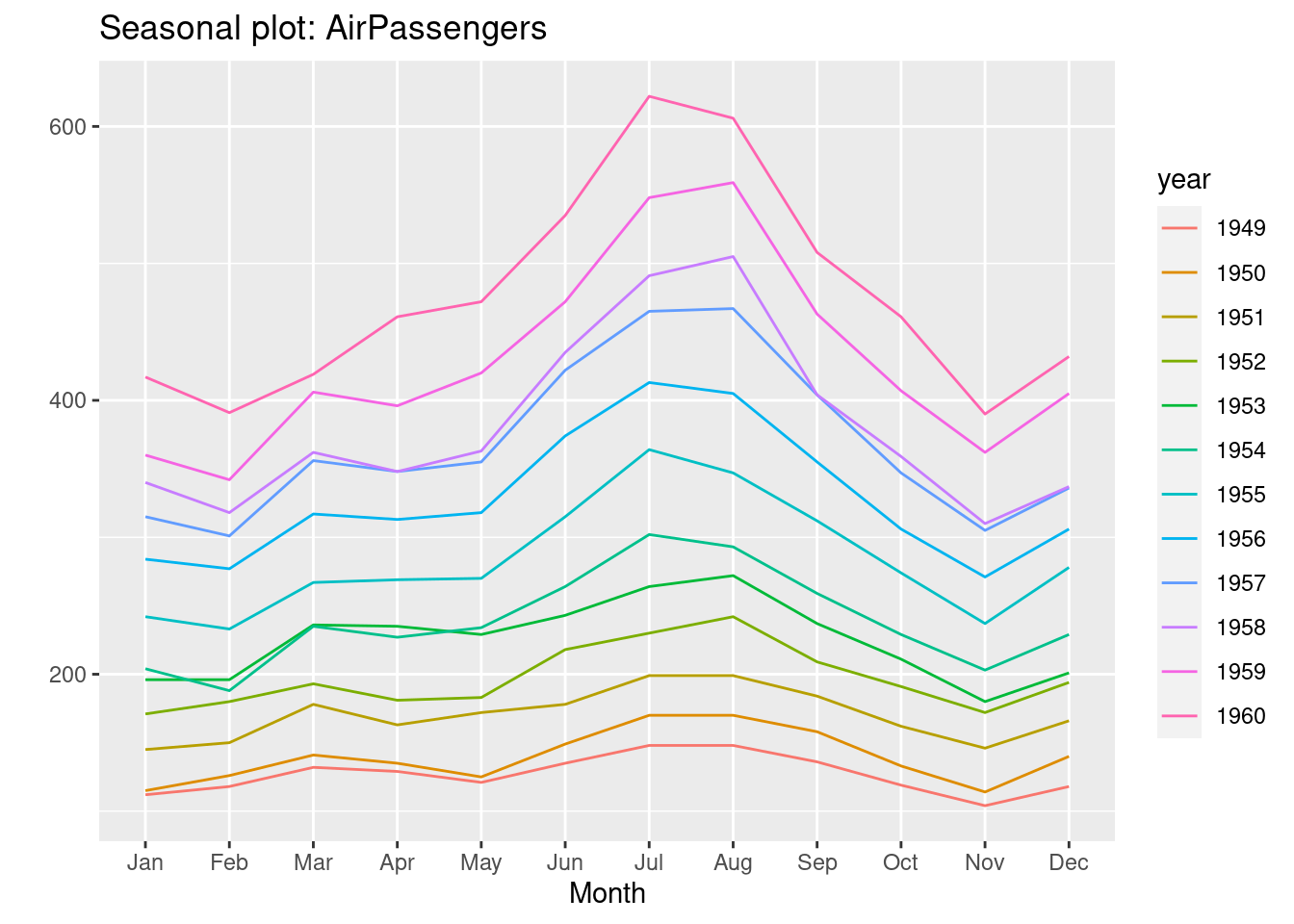

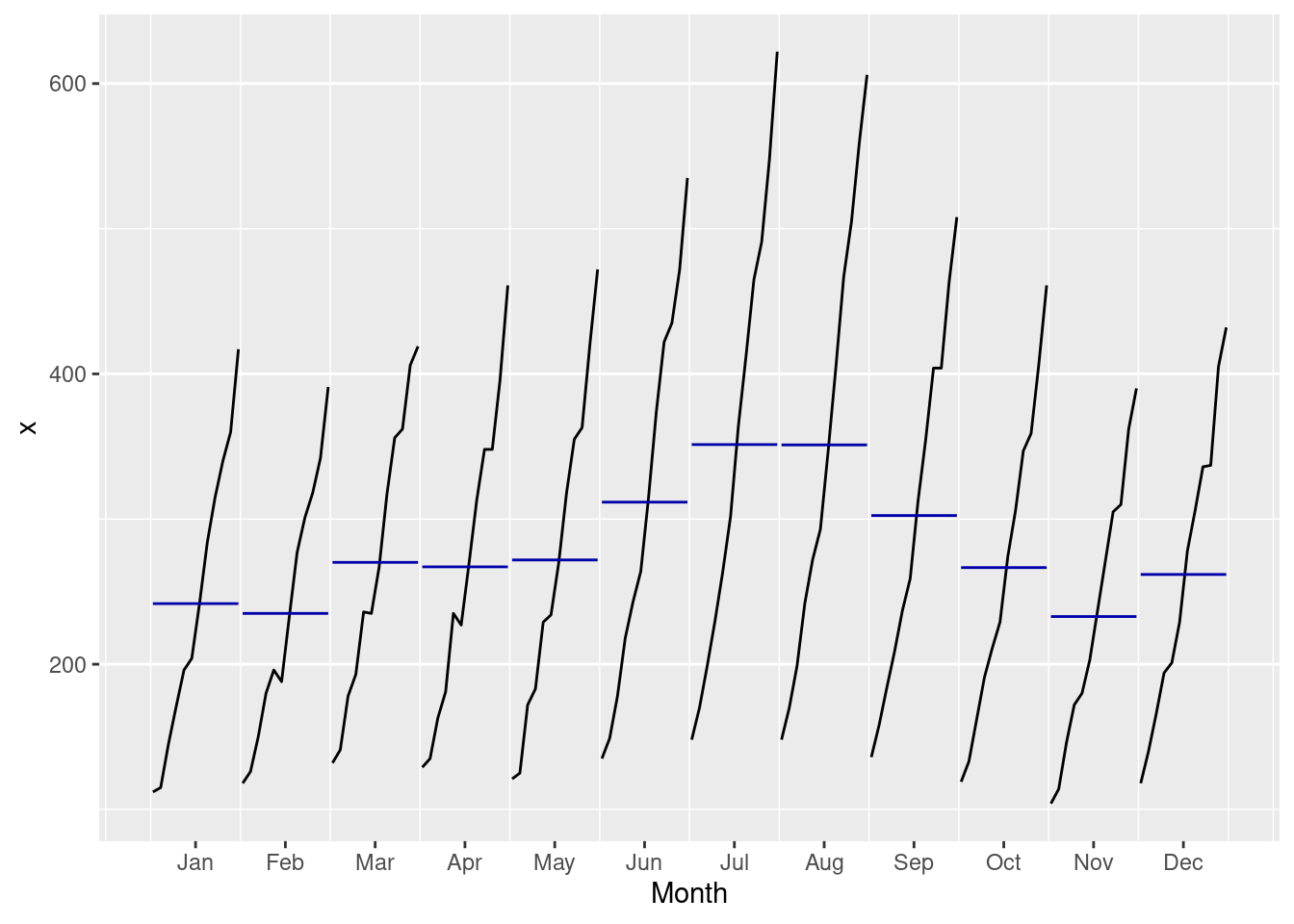

32.0.0.5.2 Using month and year creatively in line plots

- forecast package

- ggseasonplot()

- X axis is months

- Y axis is the variable of interest

- Each line represents a year.

- Shows if months exhibited similar/different seasonal patterns over the years

- ggmonthplot()

- X axis is months

- Y axis is the variable of interest

- Blue line is mean of each season

- Black line is the values for every year for a single month

- ggseasonplot()

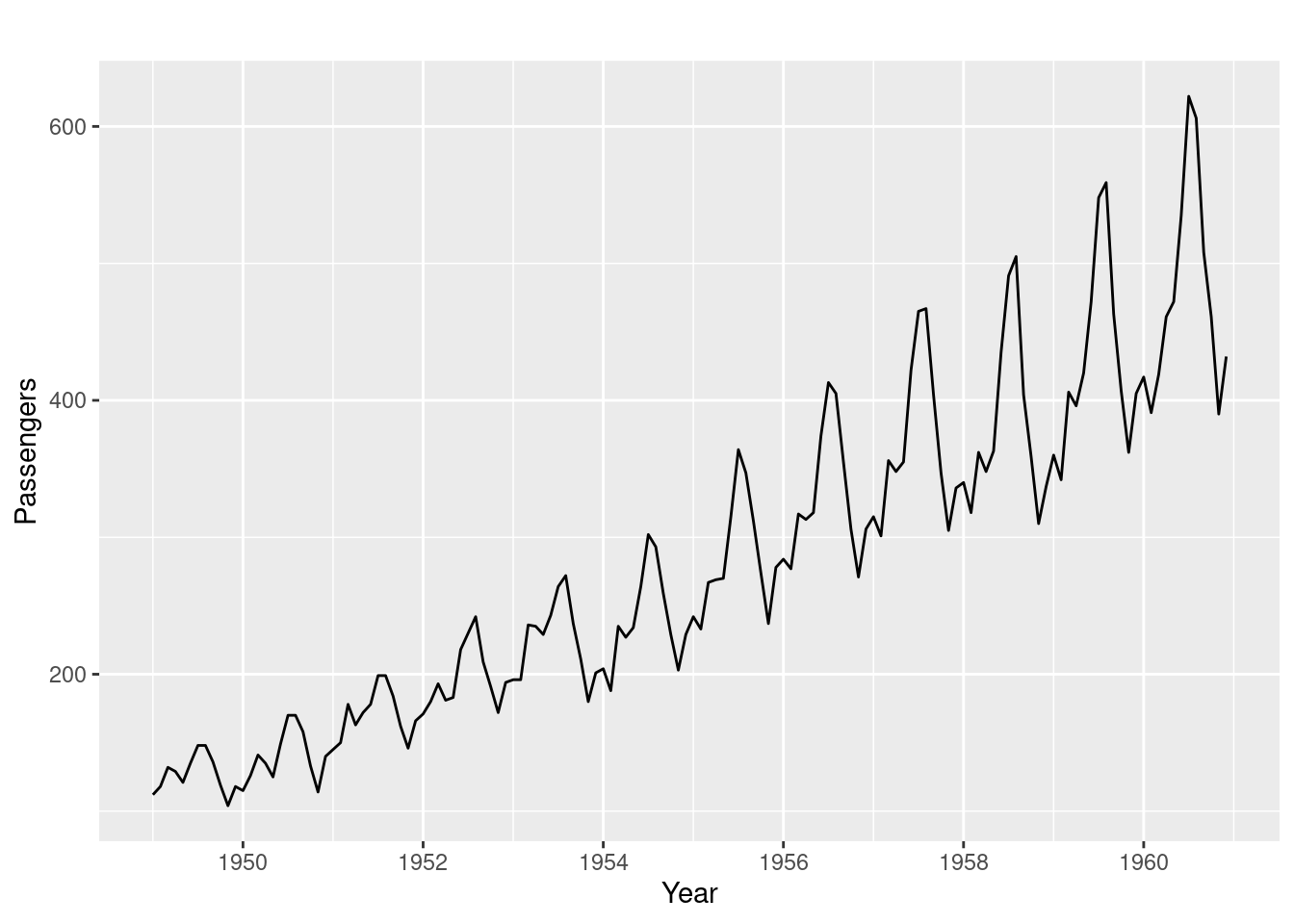

ggseasonplot(AirPassengers)

ggmonthplot(AirPassengers)

- Observations

- Some months increased more over time than others

- Passenger numbers peak in July or August

- Local peak in March most years

- Overall increase across months over the years

- Growth trend increasing (rate of increase increasing)

32.0.0.6 3-D Visualizations: plotly package

- Convert to a format plotly will understand

- Avoid using ts() object

- Dataframe with datetime, numeric columns

- lubridate package for date manipulation

- year()

- month()

new = data.frame(AirPassengers)

new$year=year(seq(as.Date("1949-01-01"),as.Date("1960-12-01"),by="month"))

new$month=lubridate::month(seq(as.Date("1949-01-01"),as.Date("1960-12-01"),by="month"),label=TRUE)

plot_ly(new, x = ~month, y = ~year, z = ~AirPassengers,

color = ~as.factor(month)) %>%

add_markers() %>%

layout(scene = list(xaxis = list(title = 'Month'),

yaxis = list(title = 'Year'),

zaxis = list(title = 'Passenger Count')))- Allows a better view of the relationship between month, year, and number of passengers

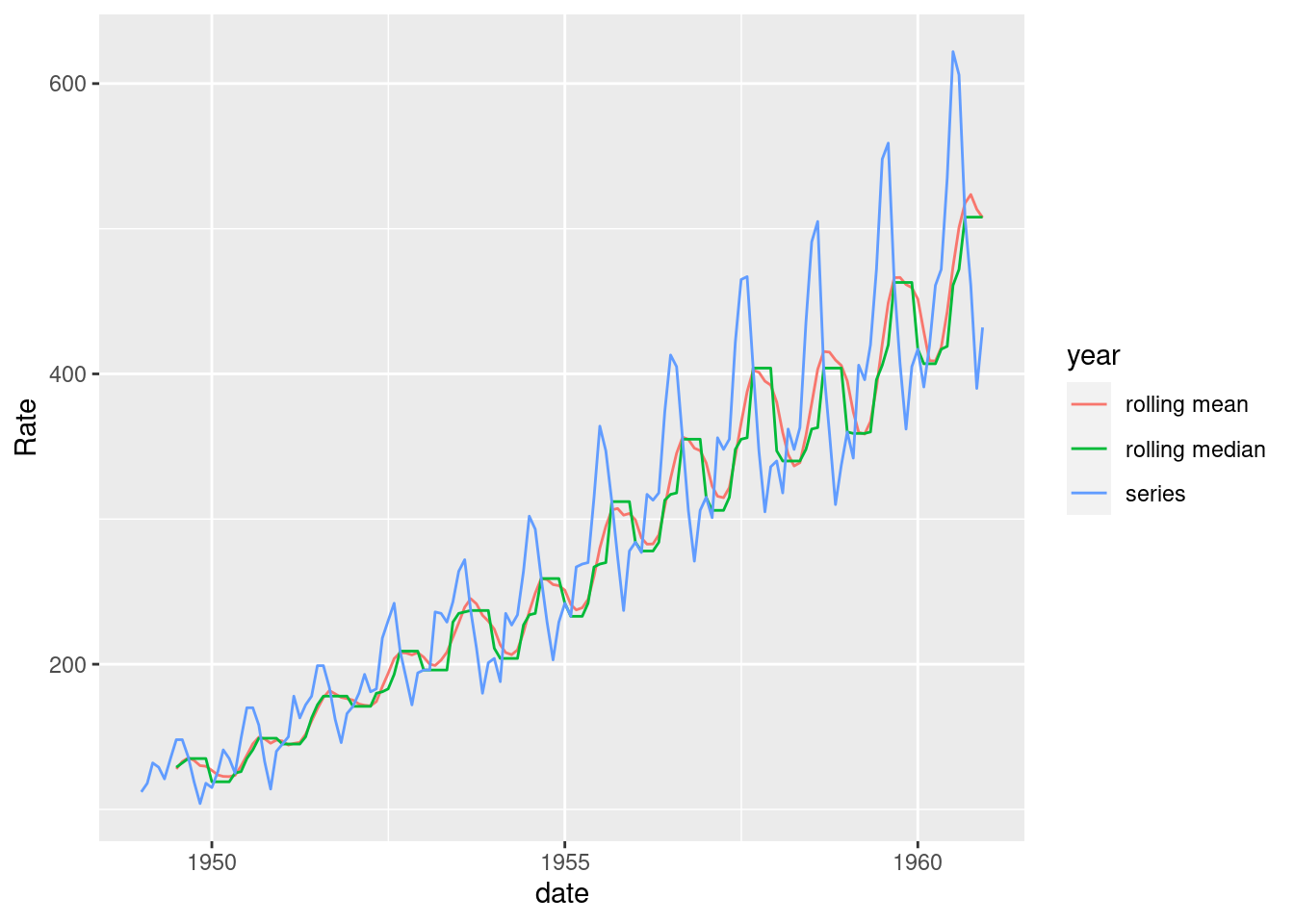

32.0.0.7 Data Smoothing

- Usually need to smooth the data before starting analysis or visualization

- Allows better storytelling

- Irrelevant spikes dominate the narrative

- Methods:

- Moving average/median

- Good for noisy data

- Rolling mean reduces variance

- Keep in mind: affects accuracy, R² statistics, etc.

- Zoo package rollmean() and rollmedian()

- k = 7 is a 7 month rolling window

- Prevent lookahead, use past values as the window (align=“right”)

- gsub() substitute series names for a clearer legend

- tidyr package gather()

- Convert from wide to long, use this as color/group in ggplot2 geom_line()

- Convert from wide to long, use this as color/group in ggplot2 geom_line()

- Exponentially weighted moving average

- Weigh past values less than recent

- pracma package movavg() function

- Useful when more recent data is more or less informative than the past

- Geometric mean

- Combats strong serial correlation

- Good for series with data that compounds greatly as time goes on

- Base R exp(mean(log())) and zoo package rollapply()

- Moving average/median

new = data.frame(AirPassengers)

new$AirPassengers=as.numeric(new$AirPassengers)

new$year=seq(as.Date("1949-01-01"),as.Date("1960-12-01"),by="month")

new = new %>%

mutate(roll_mean = rollmean(new$AirPassengers,k=7,align="right",fill = NA),

roll_median = rollmedian(new$AirPassengers,k=7,align="right",fill = NA))

df <- gather(new, key = year, value = Rate,

c("roll_mean","roll_median", "AirPassengers"))

df$year=gsub("AirPassengers","series",df$year)

df$year=gsub("roll_mean","rolling mean",df$year)

df$year=gsub("roll_median","rolling median",df$year)

df$date = rep(new$year,3)

ggplot(df[complete.cases(df),], aes(x=date, y = Rate, group = year, colour = year)) +

geom_line()

32.0.0.8 Checking Time Series Properties

32.0.0.8.1 Stationarity

- Many time series models rely on stationarity

- Stable mean/variance/autocorrelation over time

- Examine error term behavior

- Can do this visually:

- Look for seasonality, trend, increasing variance

- Statistically:

- Augmented Dickey–Fuller (ADF) test

- Null hypothesis = unit root

- Focuses on changing mean

- tseries package adf.test()

- Augmented Dickey–Fuller (ADF) test

- Visual can be better:

- ADF tests perform poorly on near unit roots, small sample size

- Use both approaches

- Remedies:

- Difference the data to correct trend

- Logarithm or square root to correct variance

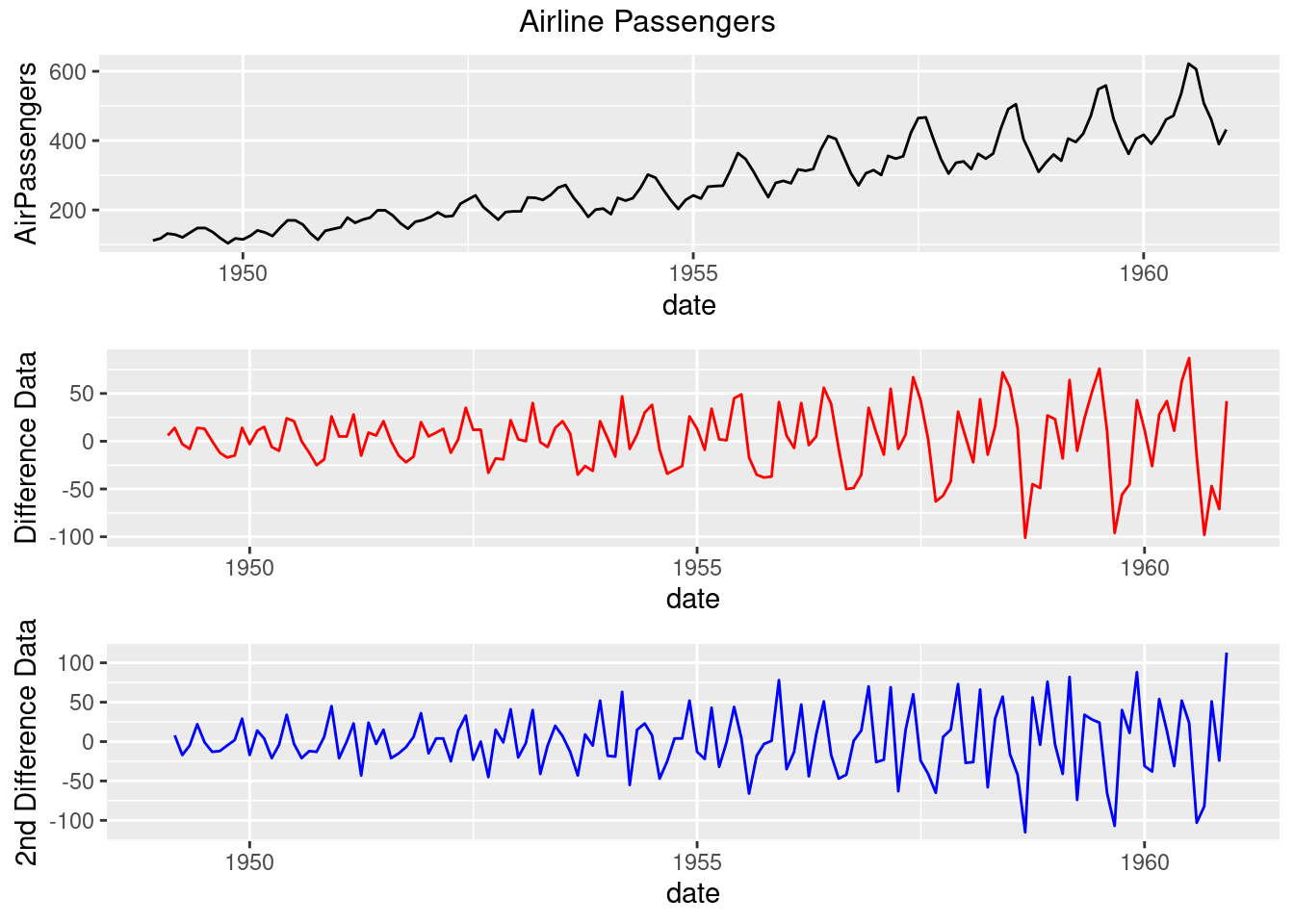

new = data.frame(AirPassengers)

new$AirPassengers=as.numeric(new$AirPassengers)

new$date=seq(as.Date("1949-01-01"),as.Date("1960-12-01"),by="month")

new$diff_data=c(NA,diff(new$AirPassengers, differences=1))

new$diff_data2=c(NA,NA,diff(new$AirPassengers, differences=2))

g=ggplot(new , aes(date,AirPassengers))+

geom_line(colour = "black")

g_diff=ggplot(new , aes(date,diff_data))+

geom_line(colour = "red")+

ylab("Difference Data")

g_diff2=ggplot(new , aes(date,diff_data2))+

geom_line(colour = "blue")+

ylab("2nd Difference Data")

grid.arrange(g,g_diff,g_diff2,top=textGrob("Airline Passengers"))

adf.test(new$AirPassengers,alternative='stationary')##

## Augmented Dickey-Fuller Test

##

## data: new$AirPassengers

## Dickey-Fuller = -7.3186, Lag order = 5, p-value = 0.01

## alternative hypothesis: stationary

adf.test(new[complete.cases(new$diff_data),3],alternative='stationary')##

## Augmented Dickey-Fuller Test

##

## data: new[complete.cases(new$diff_data), 3]

## Dickey-Fuller = -7.0177, Lag order = 5, p-value = 0.01

## alternative hypothesis: stationary

adf.test(new[complete.cases(new$diff_data2),4],alternative='stationary')##

## Augmented Dickey-Fuller Test

##

## data: new[complete.cases(new$diff_data2), 4]

## Dickey-Fuller = -8.0516, Lag order = 5, p-value = 0.01

## alternative hypothesis: stationary- Observations:

- The data has clear trend and increasing variance

- By using differencing, the trend is dampened

- There’s still some increasing variance, so log transform might be the right choice

- Things start getting muddied at second difference

- ADF says that the original series is stationary based on small p-value

- Visual inspection says otherwise

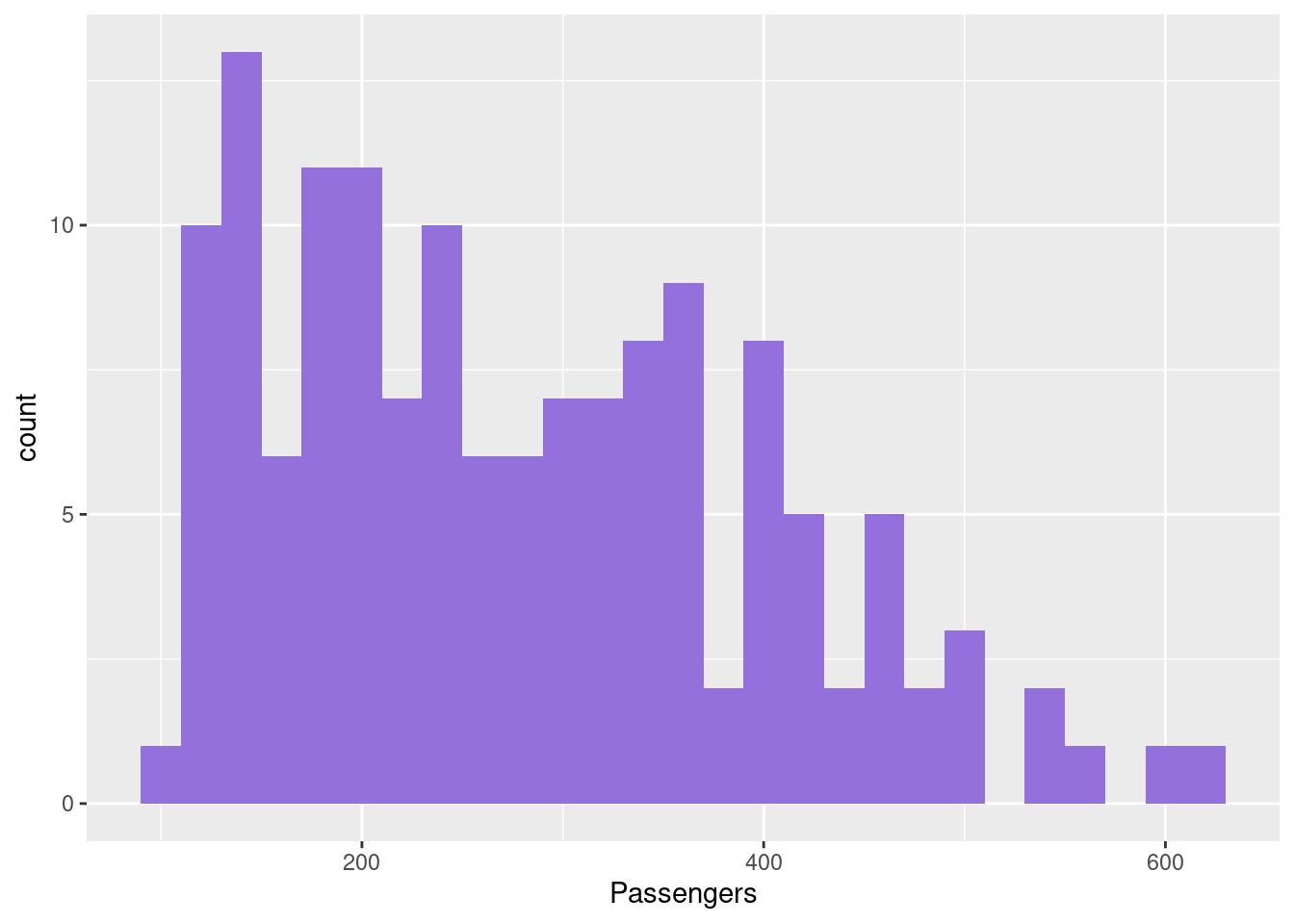

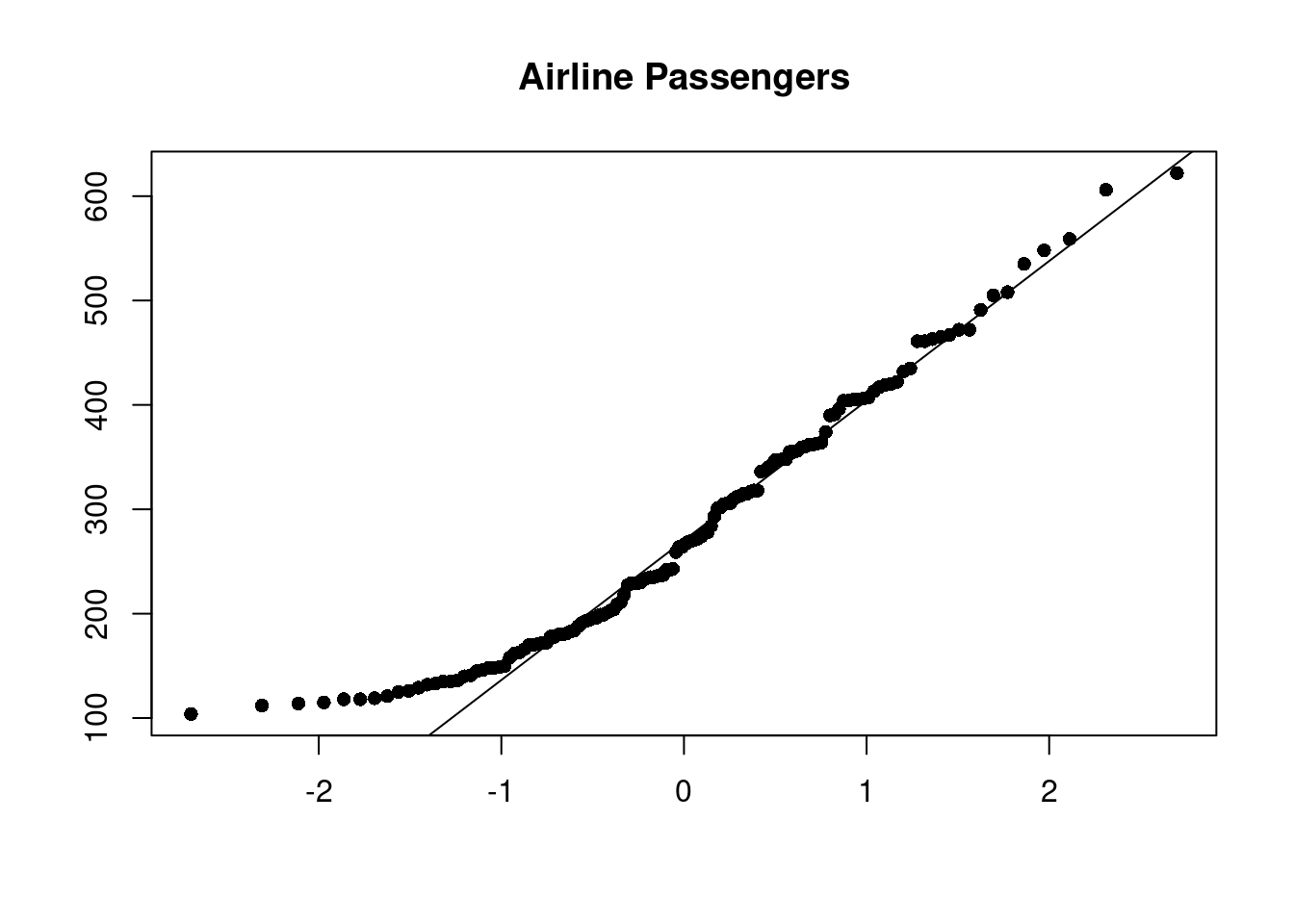

32.0.0.8.2 Normality:

- Many time series models assume normality

- This can be observed through a histogram or QQ plot

- ggplot2 package geom_histogram()

- stats package qqnorm() and qqline()

- If it is not normal:

- Box Cox transformation

- MASS package boxcox()

- Be careful with transformations!

- Are you preserving the important information?

- Box Cox transformation

ggplot(new, aes(x=AirPassengers)) +

geom_histogram(binwidth =20,fill = "mediumpurple") +

xlab("Passengers")

qqnorm(new$AirPassengers, main="Airline Passengers", xlab="", ylab="", pch=16)

qqline(new$AirPassengers)

- Observations:

- Data does not look normal: it is skewed

- Even though this doesn’t capture the time aspect of the data, the input variable must be normal for many models

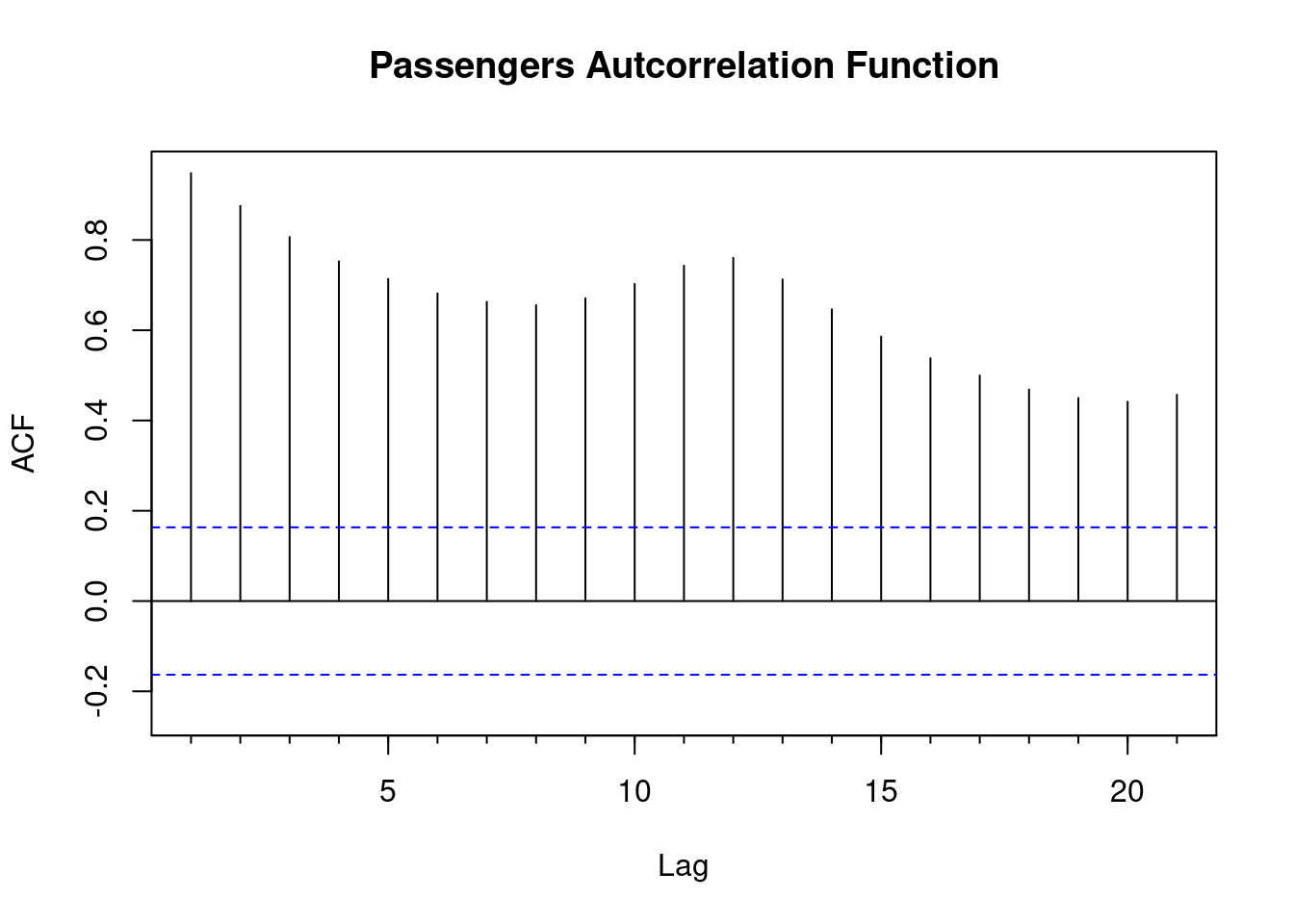

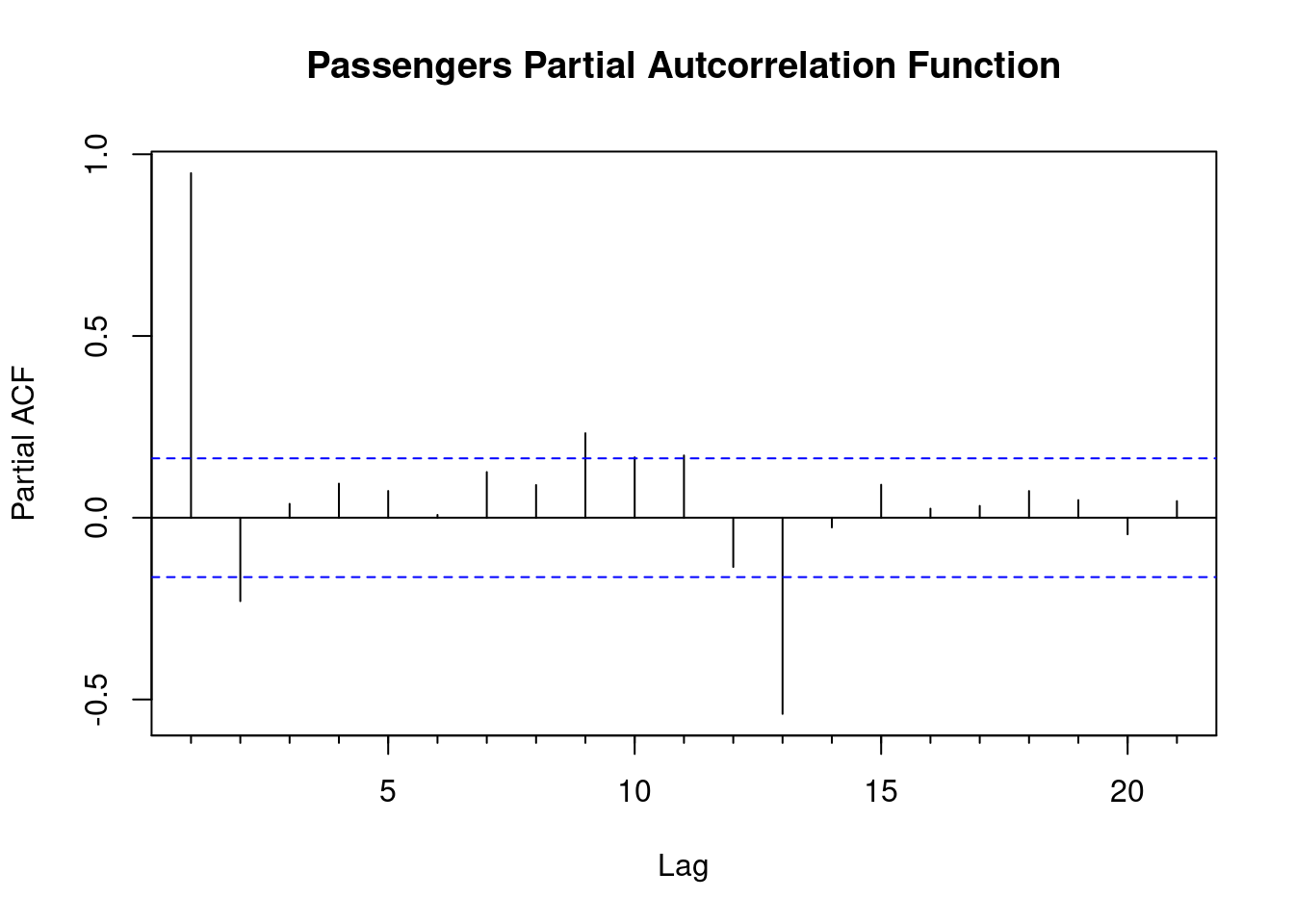

32.0.0.8.3 Lagged Correlations

- Autocorrelation Function

- Correlation between two points in a time series in a fixed interval

- Linear relationship between points as a function of their time difference

- Common behaviors:

- ACF of stationary series drops to zero quickly

- For nonstationary series, value at lag 1 is large and positive

- White noise will have 0 at all lags but 0

- Significance of ACF estimate determined by “critical region” with bounds at +/–1.96 × sqrt(n)

- forecast package Acf()

- Y axis is the correlation

- X axis is the time lag

Acf(new$AirPassengers,main='Passengers Autcorrelation Function')

- Partial Autocorrelation Function:

- The partial correlation of the series at time t with the series at time t-k given all the information between t-k….t

- Same critical regions as ACF

- ACF vs PACF:

- Redundant correlations appear in ACF

- PACF correlations show exactly how the kth lagged value is related to the current point

- PACF helps you know how long a time series needs to be to capture dynamics you want to model

- forecast package Pacf()

Pacf(new$AirPassengers,main='Passengers Partial Autcorrelation Function')

- Observations:

- The ACF fails to trail off after a certain lag, indicating clear trend

- PACF shows strong significance at around lag 12, coinciding with Christmas, a seasonal peak that is to be expected.

- Behavior of the PACF and ACF vital in determining parameters for time series ARIMA models and many others.

Now you are ready to get started with time series data!

References